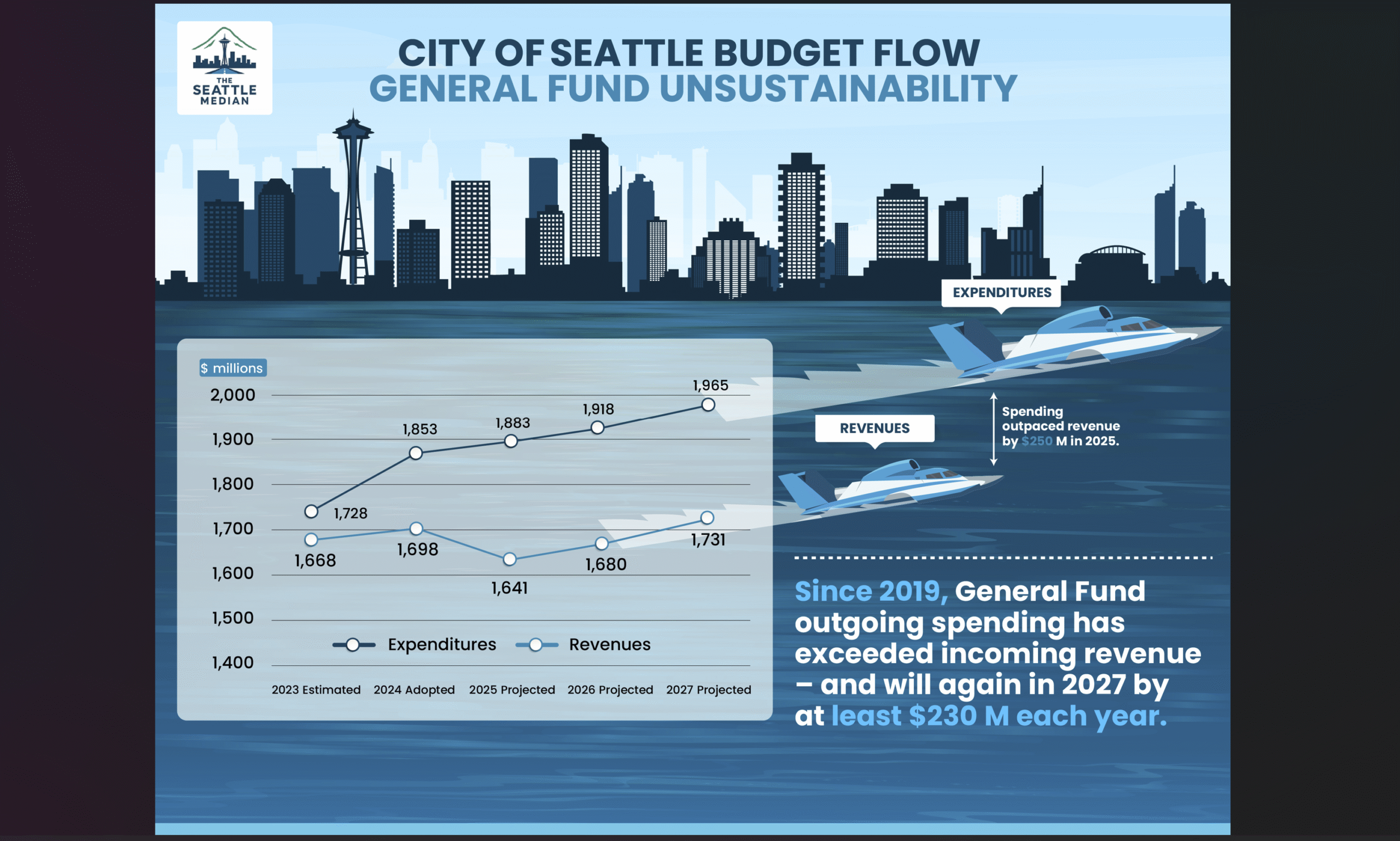

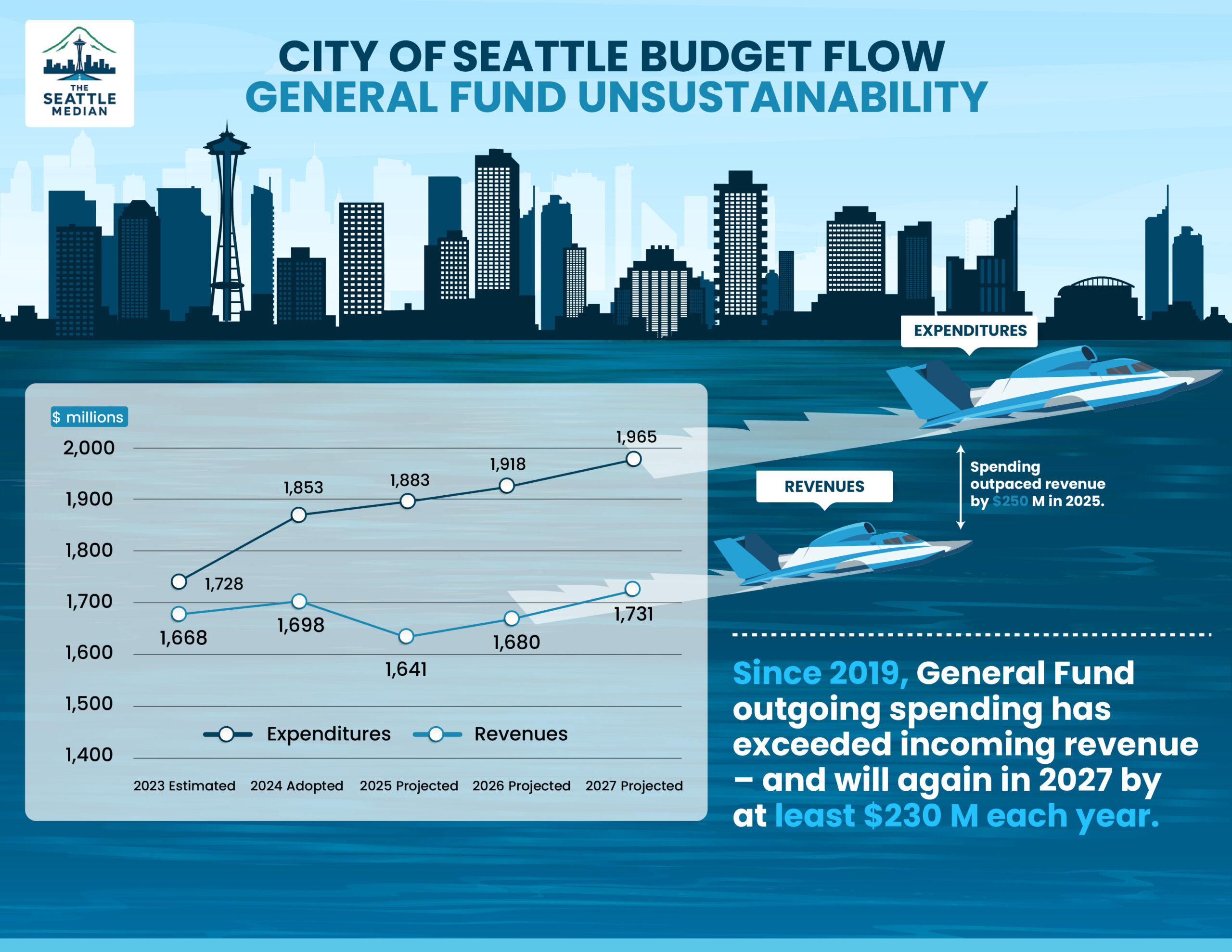

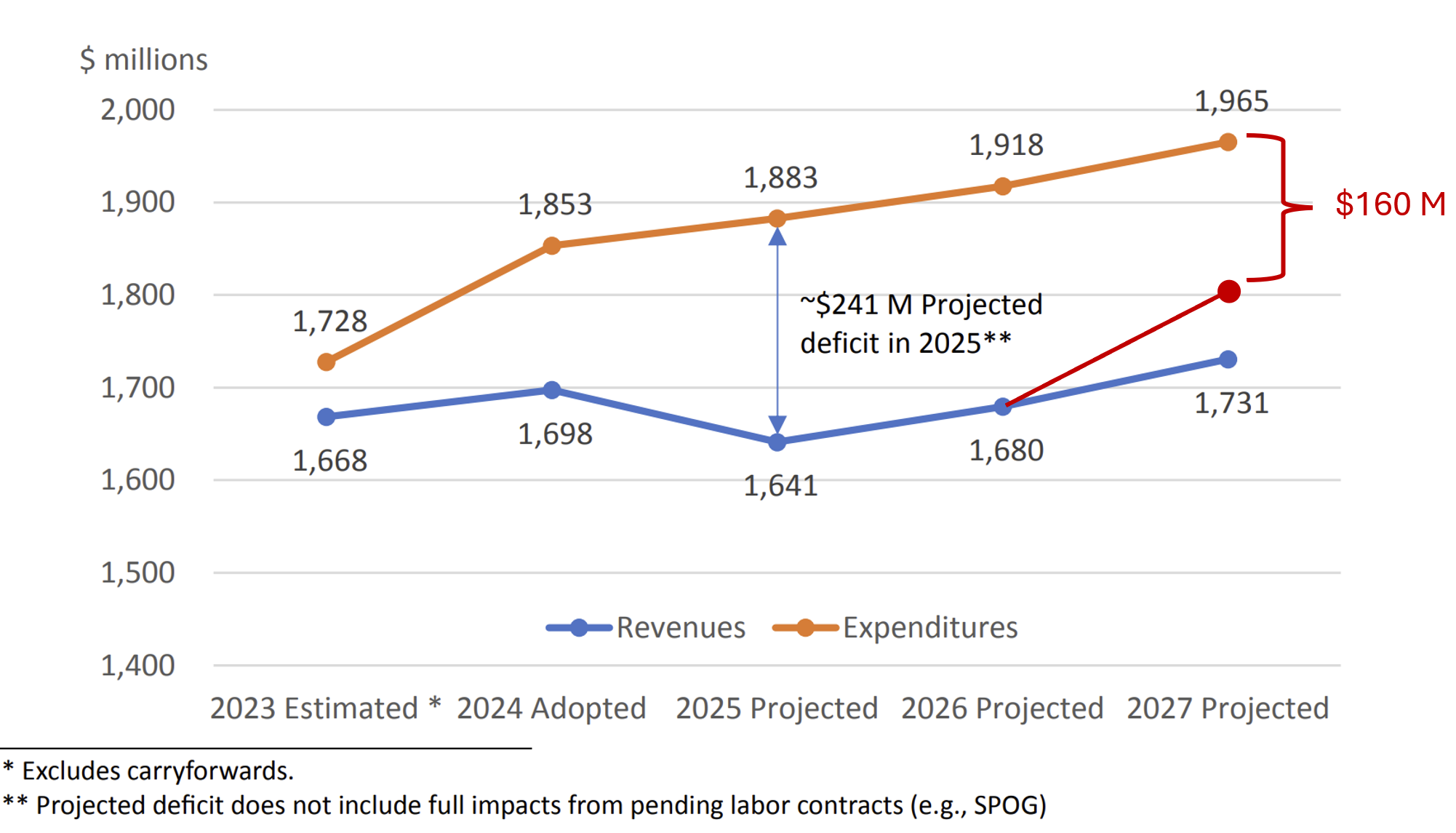

The last time spending from the General Fund was aligned with revenues coming into the General Fund was 2019. Since then spending going out of the General Fund has exceeded revenues coming into the General Fund by ever-increasing amounts, reaching $241 million in 2025.

In the 2023 and 2024 budgets, the City used one-time measures to close this gap, including using fund balances from the prior year, fiscal reserves, federal grants, and other maneuvers.

But mostly they raided the Payroll Expense Tax Fund. As we pointed out in earlier post, the Payroll Expense Tax was meant as a dedicated funding source mostly for affordable housing. Now it’s mostly a fund to backfill the General Fund.

As the Mayor’s Office notes, “Each year since enacting the payroll tax in 2020, the City has balanced the General Fund using a “temporary” allocation of payroll tax revenues. Each of these decisions was made for a one-year period, with the assumption that the payroll tax would no longer be used for this purpose in the following year.”

But that assumption appears to be no longer held.

To address the $241 million gap between incoming revenues and outgoing spending in the 2025 budget, the City diverted $305 million in tax revenues from the Payroll Expense Tax Fund, which represented the largest expenditure from the $516.66 million fund.

Following the budget’s adoption, City budget leaders began including the Payroll Expense Tax Fund in with the General Fund in their General Fund revenue projections, although they are separate funds. Even with this change to count the General Fund and the Payroll Tax as a combined resource, the General Fund is projected to spend $233 million more than revenue coming in, beginning in 2027.

The Council proposed and unanimously approved a “rebalancing” of the City B&O tax, which has been signed by the Mayor is projected to raise $80 million per year if approved by voters.

Even if we adjust the revenue line from $1.73 billion to $1.81 billion to reflect the additional $80 million per year, there is still a deficit of around $160 million.

The question remains: How long can the City of Seattle continue to operate on one-time fixes, accounting maneuvers, and unsustainable measures? What would it take for the City to reckon with fiscal reality? What will happen if it doesn’t?

We’ll take up these questions in future posts.