In our first series of posts, we looked at the state of the City of Seattle’s budget and the increasing reliance on the Payroll Expense Tax, also known as the JumpStart Tax, for backfilling the General Fund.

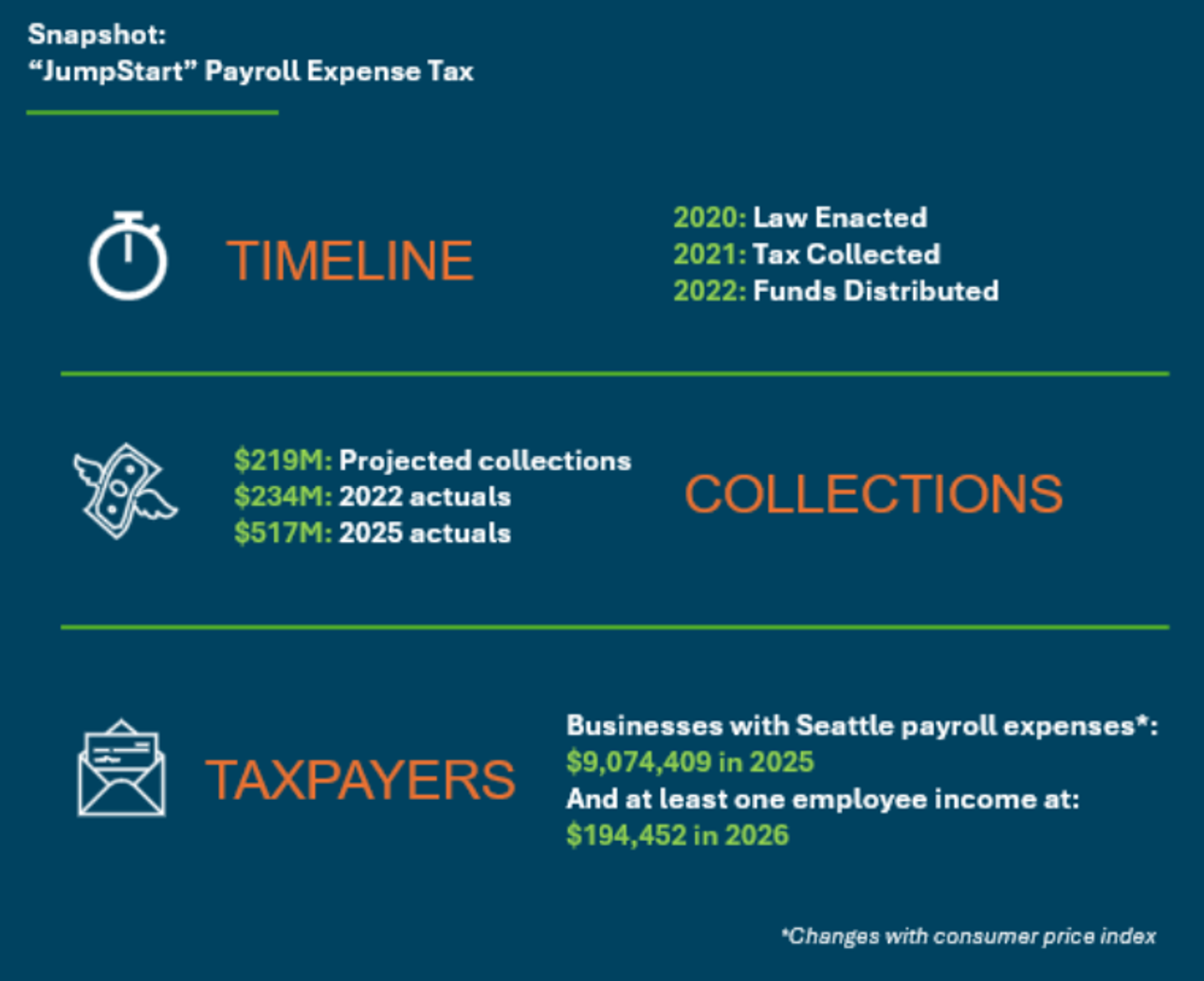

First, a definition: the Payroll Expense Tax levies a tax on Seattle’s largest businesses, which include employees that meet an income threshold. This threshold changes with the consumer price index.

Here’s a snapshot of the law, by the numbers (all budget data derived from the city’s Open Budget portal):

What’s the purpose of the Payroll Expense Tax?

When the Payroll Expense Tax was drawn up in the summer of 2020, its chief sponsor framed the tax as a response to “the immediate COVID crisis” and a tool for long-term economic revitalization, with a focus on affordable housing and essential city services, according to a press release.

In 2022, the City Council passed a revision to more specifically direct how ongoing collections would be distributed, with 62 percent dedicated to affordable housing, about a third spread across economic revitalization, equitable development and environmental initiatives, and five percent for administration.

Yet, as we pointed out, the City immediately began accessing the fund as a “temporary” source for backfilling the General Fund. As the Mayor’s Office noted, “Each year since enacting the payroll tax in 2020, the City has balanced the General Fund using a “temporary” allocation of payroll tax revenues. Each of these decisions was made for a one-year period, with the assumption that the payroll tax would no longer be used for this purpose in the following year.” In 2024, that “temporary” mechanism became permanent, with a Council vote to loosen constraints on JumpStart spending to more categories including the General Fund.

Critical of the move were affordable housing advocates, who argued for continued budgetary guardrails that maximize resources for the City’s housing crisis.

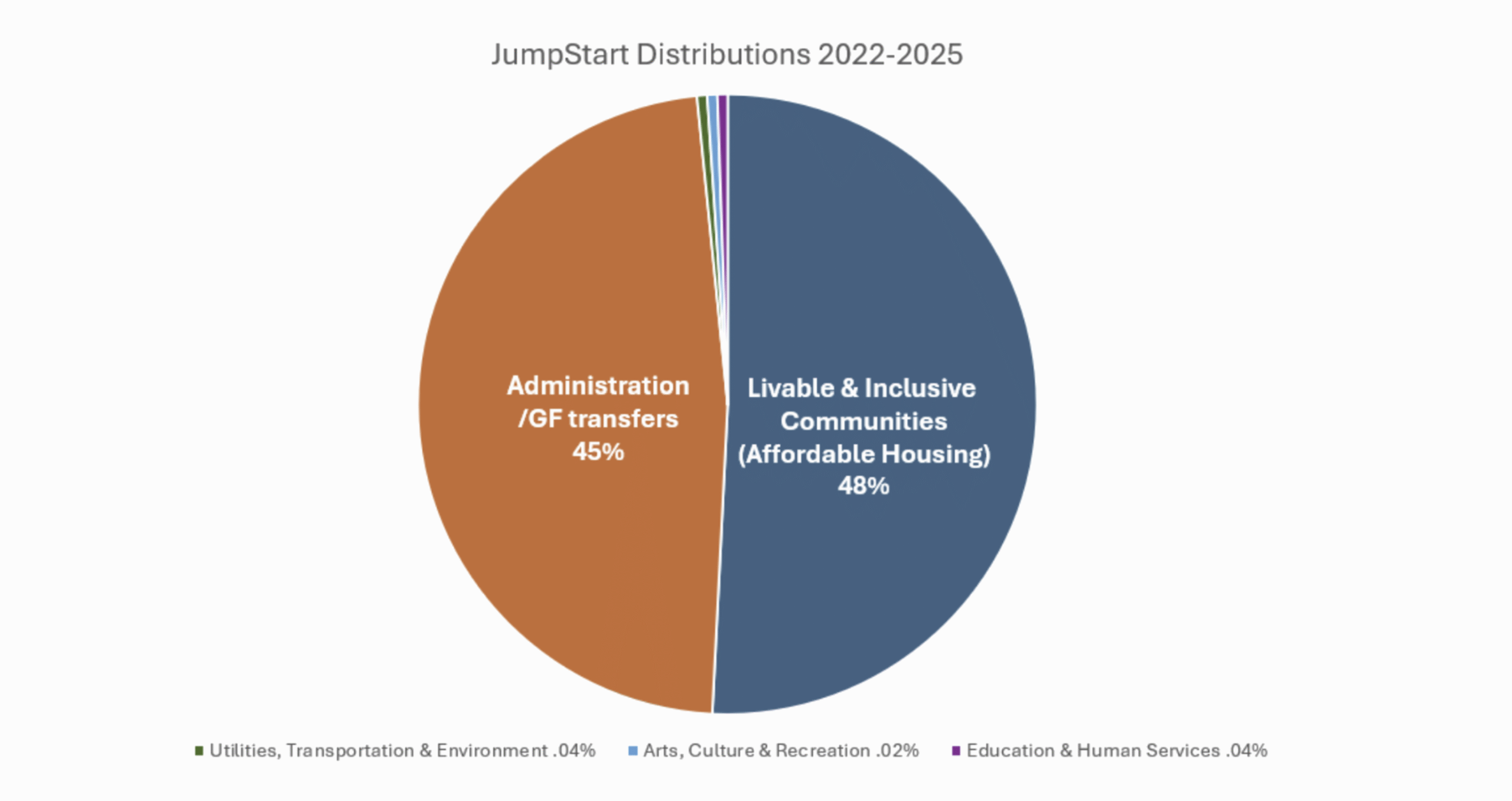

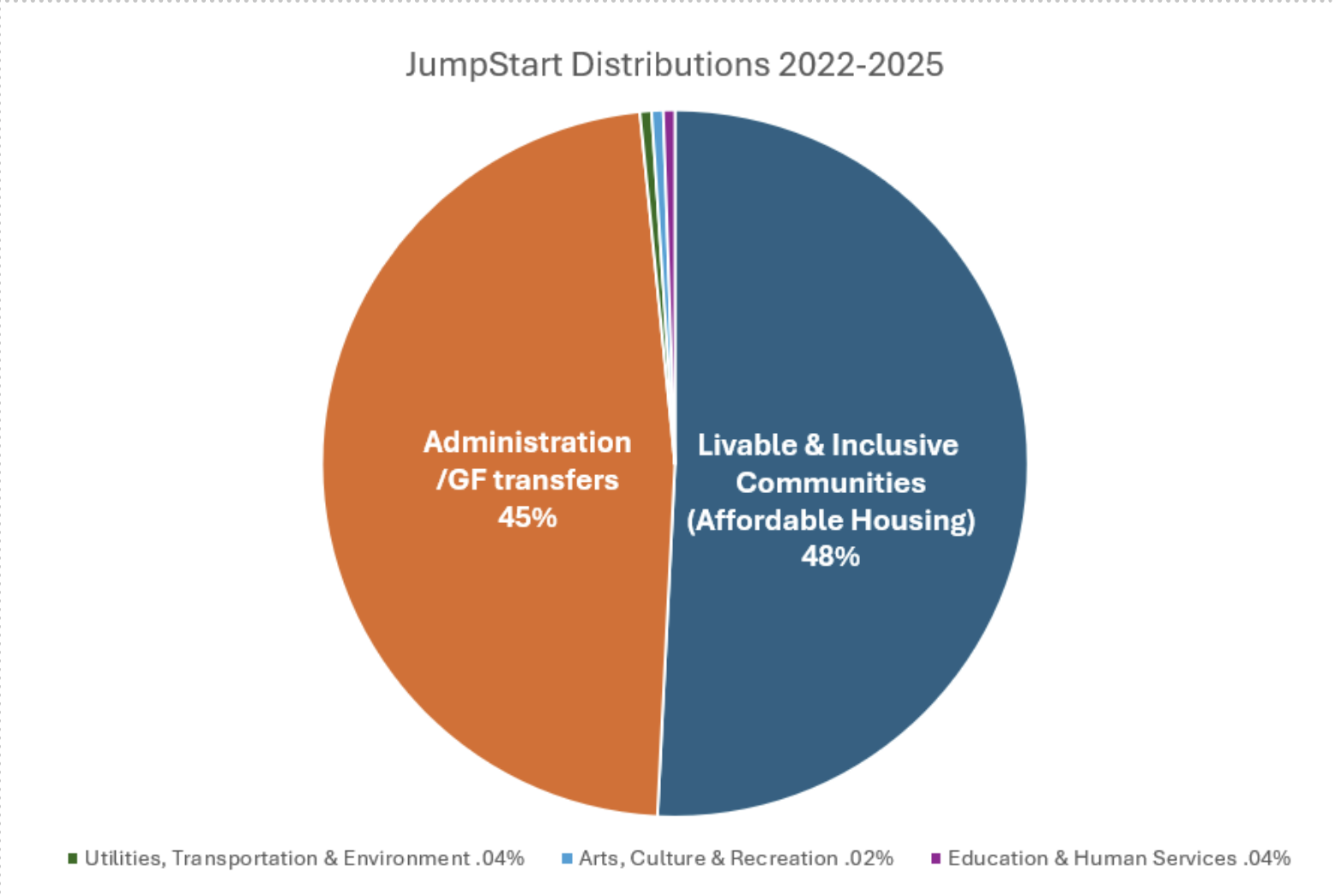

Over the first four years of JumpStart distributions, here’s how city leaders have allocated funds.

Why do distributions diverge from the law’s stated intent?

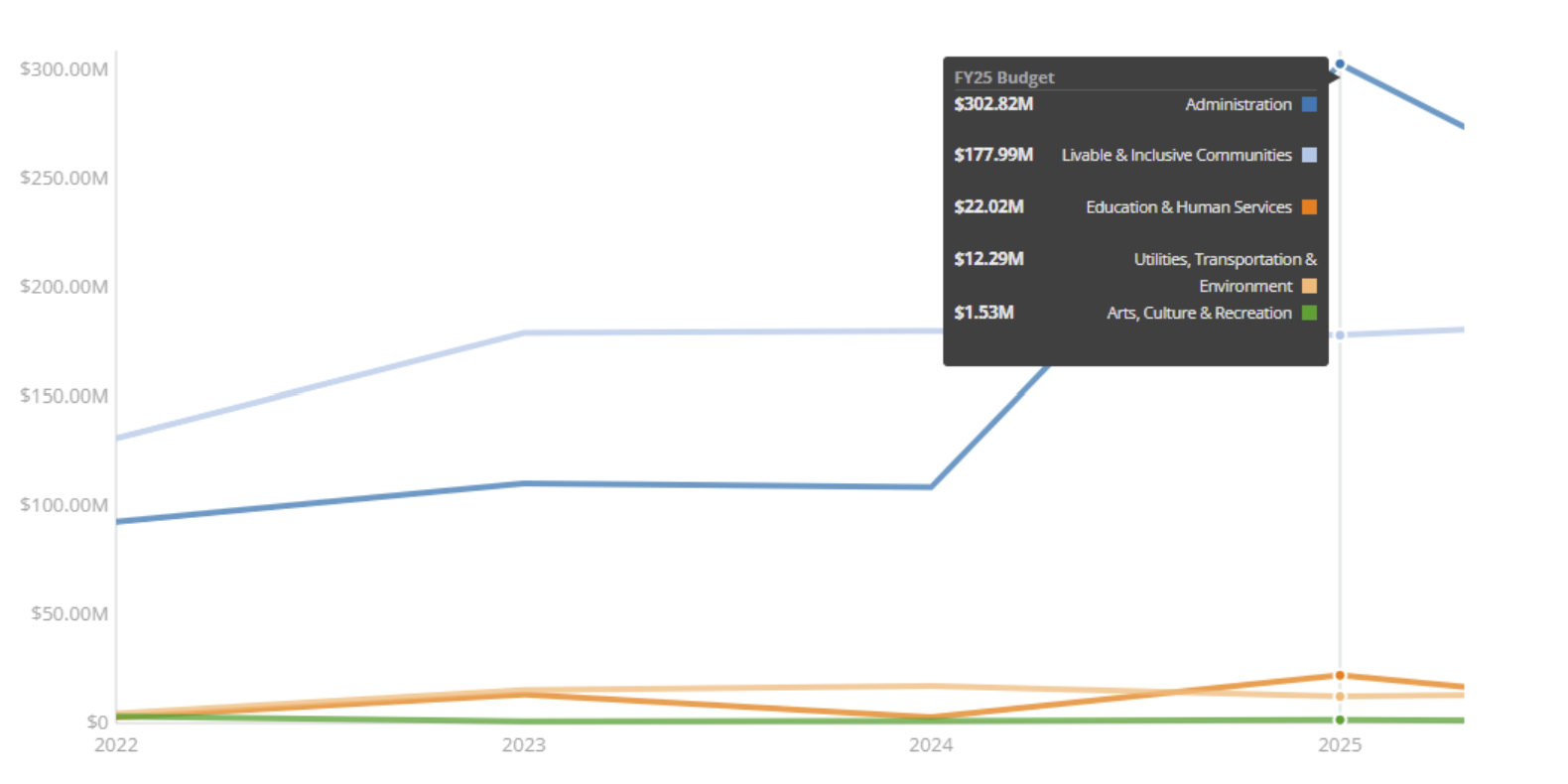

JumpStart tax collections have far outpaced projections. As the revenue has grown, the money distributed for its original purposes (i.e., housing) has remained relatively consistent year over year, while city leaders have redirected overages to backfill the General Fund.

This chart from the City’s Open Budget portal illustrates that shift:

Why did tax collections balloon?

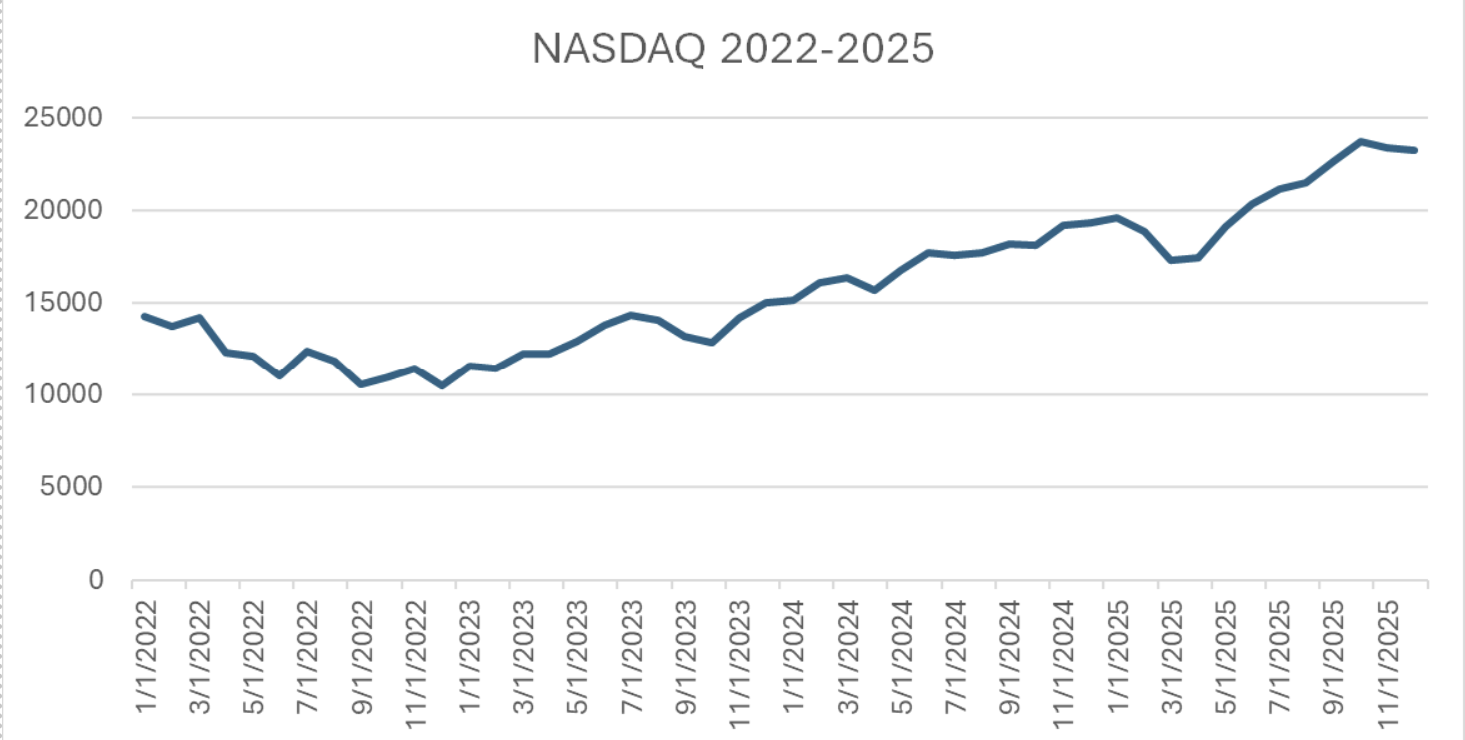

Seattle’s largest employers often compensate employees with stock-based pay. As the stock market rises, so do reported incomes—and Payroll Expense Tax collections. Employers like Amazon, Starbucks and Microsoft are all on the NASDAQ, which grew 55% between the end of 2022 and the end of 2025.

In downturns, the inverse applies, leaving City revenues vulnerable. A 2024 City revenue report shows about 70% of JumpStart revenues are generated from just ten companies, creating “significant inherent volatility in this revenue stream.”

What’s next?

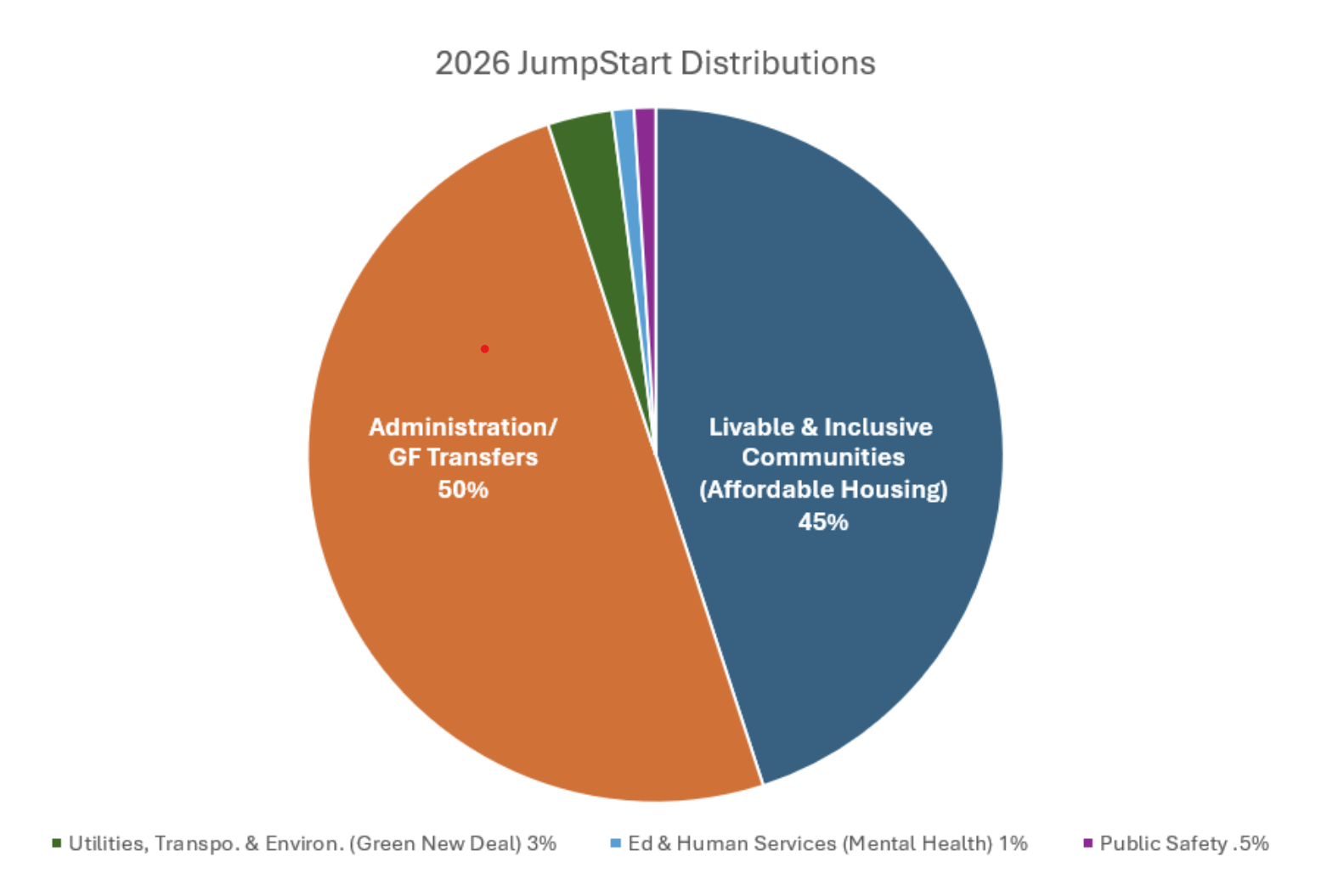

The 2026 budget, proposed by former Mayor Bruce Harrell and approved by the City Council last year, includes $416 million from the Payroll Expense Tax Fund.

Here’s how the city will direct that funding.

In future years, recently installed Mayor Katie Harrell will bring fresh perspective to the budgeting process, but the underlying challenges will sound familiar.

The General Fund is facing ongoing deficits: $140 million in 2027, $268 million in 2028, and $373 million in 2029, according to the previous mayor’s budget. Meanwhile, the Payroll Expense Tax is starting to hold flat, topping out just over $400 million each year.

With JumpStart revenues flattening and structural deficits growing, the numbers suggest the tax can no longer carry both long-term investments and budget stabilization without forcing a broader reckoning in Seattle’s budget.