Seattleites have a right to know if the policies they’ve supported are actually delivering on their promises. How can we determine if the policies Seattle has enacted are achieving their intended goals? These are the questions at the core of good governance. The City’s budget, often presented as a straightforward financial document, is the first place to look for answers.

But a closer examination invites more questions. Do the City’s priorities align with voters’? Is the spending sustainable? Is the City transparent about where the money goes? Does it report on whether programs are having success?

This overview of the City of Seattle’s budget addresses key questions:

- How big is the budget and how has it grown over time?

- Where does the money come from?

- Where does it go and what is it paying for?

- Is the budget sustainable?

The most important question of all is this: Is it working? Future posts and analysis will delve deeper into specific policy areas, analyzing not just the financial aspects but also the goals and measurable outcomes associated with them. What’s working? What isn’t?

Operating budget

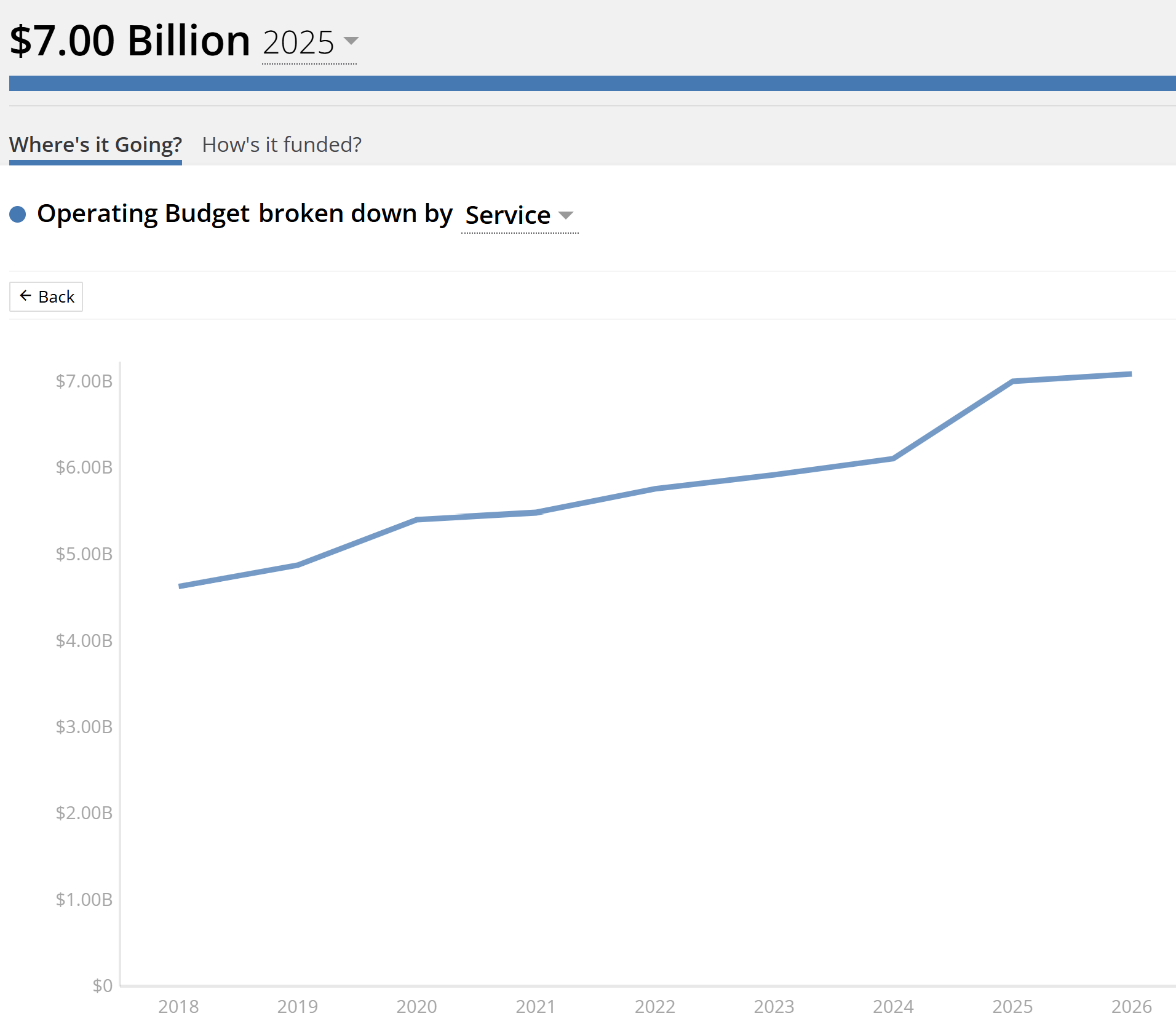

The City of Seattle’s 2025 operating budget is $7 billion. The City’s Open Budget portal provides historical data back to 2018. For example, the operating budget in 2025 is 51% greater than the $4.63 billion operating budget in 2018.

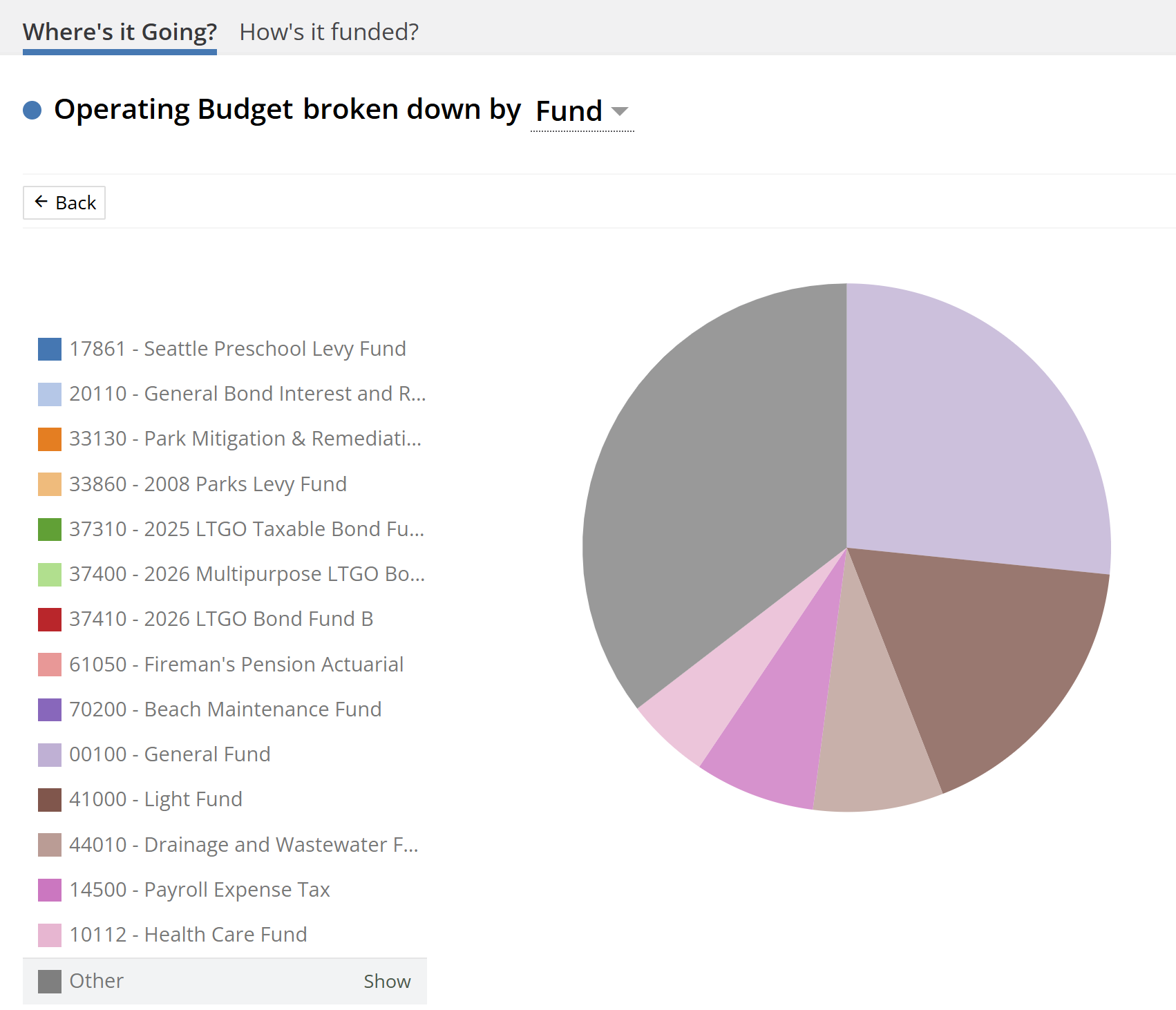

Open Budget organizes this data in several ways – by fund (cash coming in), by department (cash going out), and by program and service (what the cash is paying for).

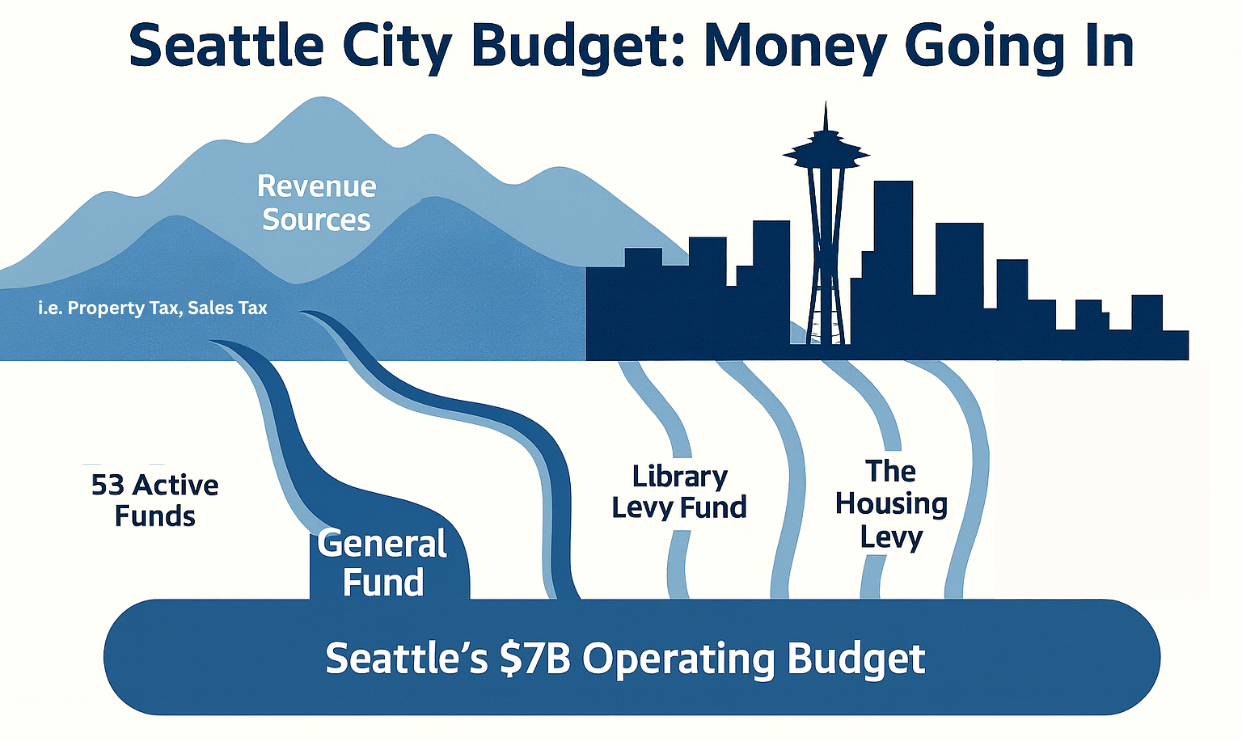

The Cash Coming In

Restricted Funds

There are 53 active funding sources for the 2025 operating budget that we (taxpayers, collectively) contribute to in a variety of ways. These include:

- User fees that show up on our utility bills, which fill the Light Fund, the Water Fund, the Solid Waste Fund, etc.

- Property tax levy lid lifts that we’ve approved, which fill specific funds for specific uses (i.e. the Families Education Preschool Promise Levy, the Library Fund, etc.)

- Municipal bonds

- State and federal grants

These funds are restricted, meaning utility fees go to utilities, Library Fund revenues go to libraries, etc.

The General Fund

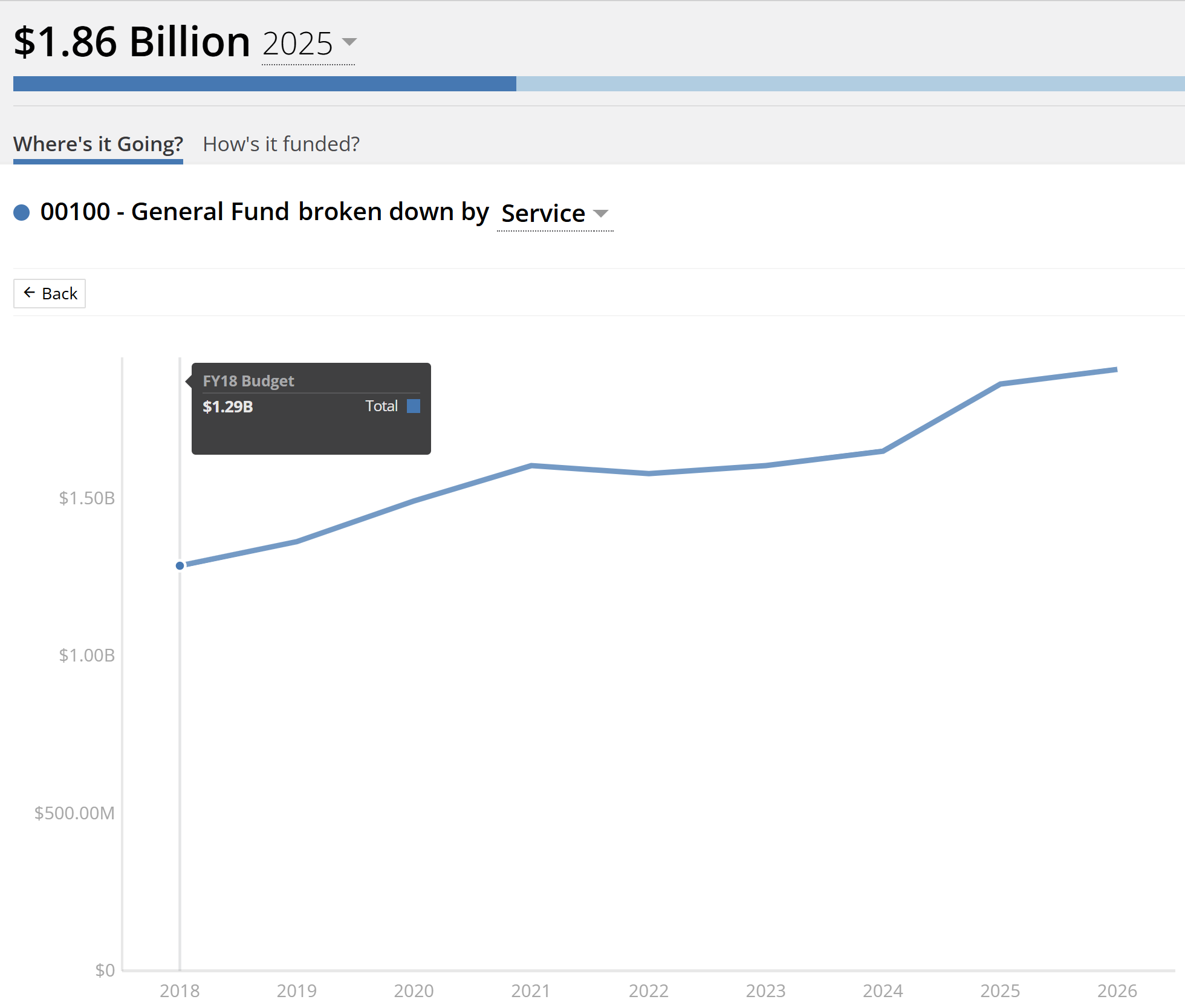

The primary exception is the General Fund, which you can see above is the largest of all funds at $1.86 billion, or 26.6% of the operating budget. The General Fund can also be tracked back to 2018, when it stood at $1.29 billion.

The General Fund is the one we most often hear debated at City Hall because it’s unrestricted. That means its revenues are flexible and can be redirected by our elected officials.

It’s also the fund where the cost of the programs it pays for have exceeded the revenue it receives since 2019 (more on this in a future post).

General Fund revenues are primarily fueled by property, retail sales, utility, and business & occupation (B&O) taxes, all paid by hardworking Seattle residents and businesses.

Payrolls Expense Tax Fund

Another exception is the Payroll Expense Tax Fund, which is funded by a tax on employees of large businesses, also known as the JumpStart Tax. This tax was enacted in 2020 as a dedicated funding source mostly for affordable housing, with other investments in tourism, equitable economic development, and the Green New Deal.

However, every year since it’s been enacted, because of the spending challenges in the General Fund references above, an increasing portion Payroll Expense Tax has been diverted into the General Fund to allow it to balance (more on this below.)

Here’s a look at the basic flow of funds into the operating budget.

Now we’ll take a look at how the Operating Budget allocates these dollars.

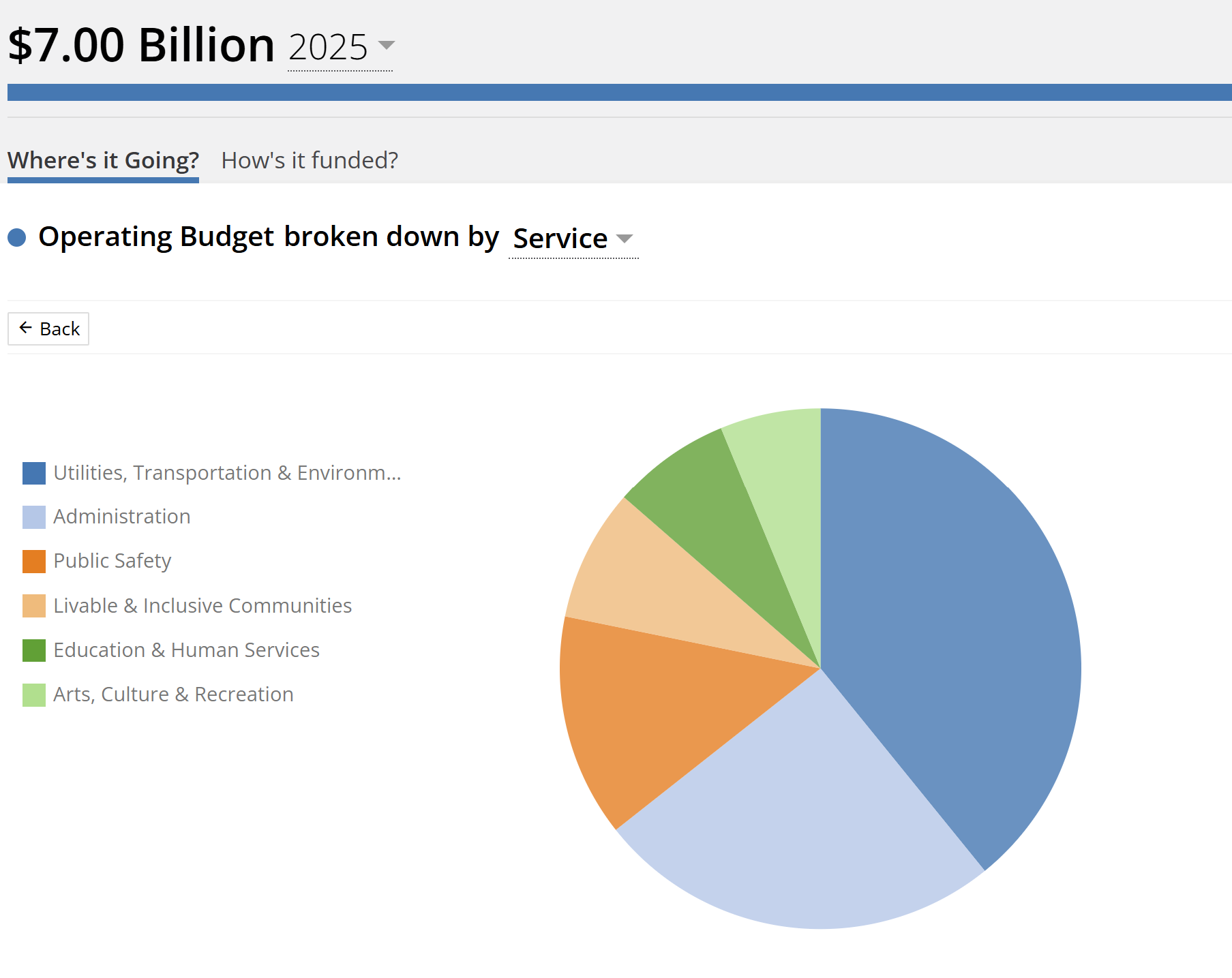

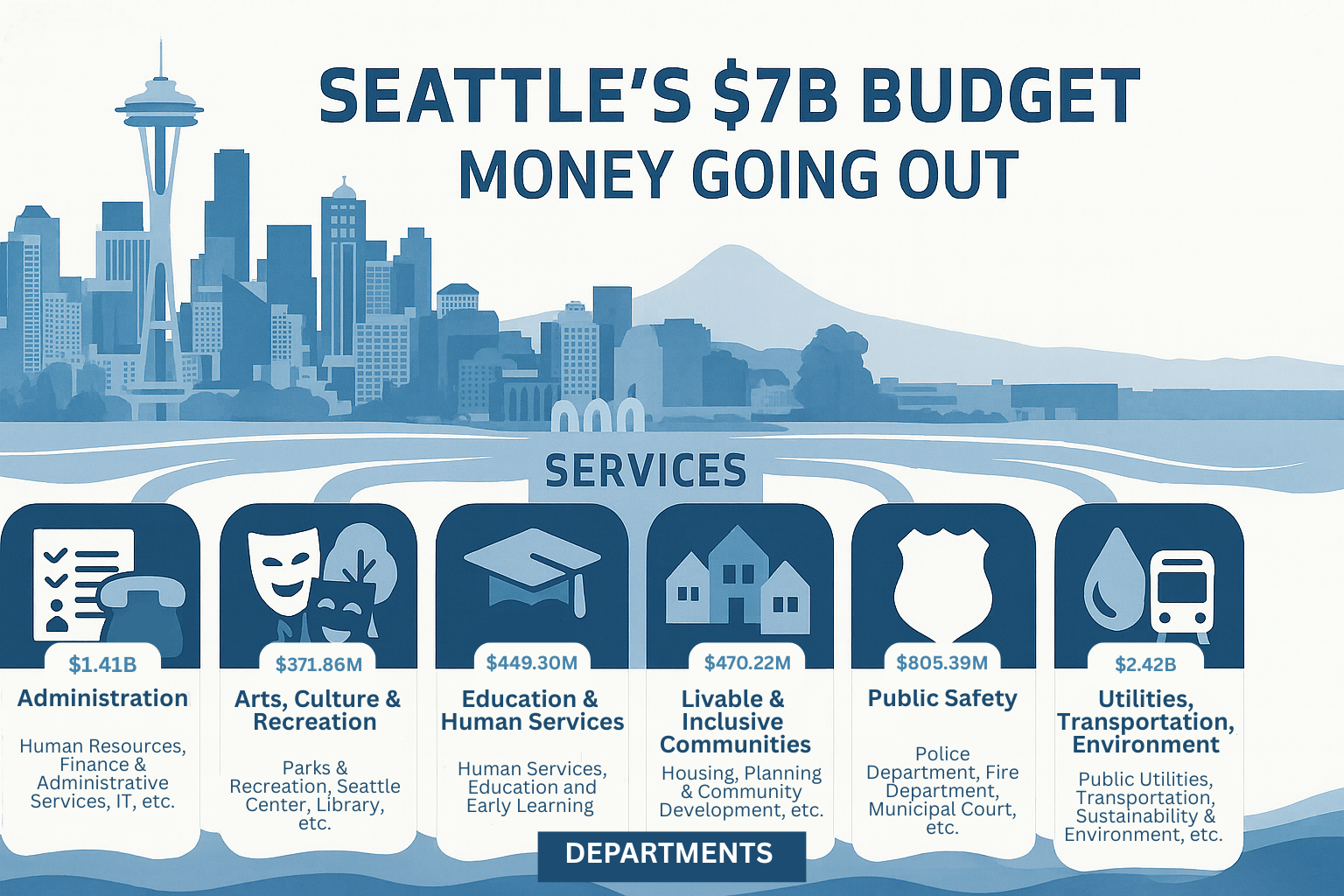

Where the Cash Goes: Service Areas

The Budget Office breaks the operating budget into six major policy buckets and tracks their growth over time, with the City’s 44 departments grouped within one of these policy areas. They are:

- Administration ($1.41 billion): Human Resources, Finance & Administrative Services, IT and more

- Arts, Culture & Recreation ($371.86 million) Parks & Recreation, Library, Seattle Center, Arts and Culture and more

- Education & Human Services ($449.30 million) Human Services, Education and Early Learning and more

- Livable & Inclusive Communities ($470.22 million) Housing, Construction and Inspections, Planning and Community Development and more

- Public Safety ($805.39 million) Police Department, Fire Department, Municipal Court and more

- Utilities, Transportation, & Environment ($2.42 billion) Public Utilities, City Light, Transportation, Sustainability and Environment and more

You can see a full list of departments by policy area in the table of contents of this City Council report.

Where the Cash Goes: Department

Open Budget’s breakout by department shows each City department’s budget and its percentage of the operating budget (these can also be tracked year-over-year back to 2018).

City Light, for example, owns largest single share of the operating budget pie, at 17.46%. Seattle Public Utilities is second largest, at 16.5%. This is why the Utilities, Transportation & Environment policy area represents nearly 40% of the operating budget.

The funding for each department varies. City Light is self-funded, receiving 100% of its funding from the Light Fund, with revenues entirely generated from residential, commercial, and industrial electric power sales.

The Seattle Police Department receives all (99.2%) of its funding from the General Fund. Same with the Fire Department.

Parks & Recreation is an example of a department with multiple funding sources, with half of its funding coming from the General Fund and the remainder coming from 6 other funds, including the voter-approved Park District Levy. Clicking on the Park District Levy allows you to see the programs funded this specific revenue source.

What the Cash is Paying for: Programs

Which brings us to programs. Every department provides of view a how each departmental budget is allocated by program. For example, you can see that the Office of Housing spends nearly 73% of its $343.43 million budget on multifamily lending.

From here, you may want to drill down into how a particular program is funded. Funding for the multifamily lending program, for example, is split between the Low Income Housing Fund (two-thirds of the program) and the Payroll Expense Tax (one-third of the program).

A click on the entire operating budget by program shows appropriations by program, from largest to smallest:

- The single largest appropriation by program is Debt Service, at $514.3 million – 7.3% of the operating budget.

- Appropriation to Special Funds is the next item, which represents fund transfers.

- Departmental Indirect Costs – overhead costs, in other words – accounts for $489.8 million, or 7% of the budget.

- Health Care for City employees costs $362.4 million, or 5.2% of the budget.

- Citywide Indirect Costs – more overhead – accounts for $279.7 million, or 4% of the budget.

You have to go eight lines down the largest expenditures in the operating budget before you reach an expenditure that does not directly fund the infrastructure of City government and is instead a program that Seattleites can access; this is the multifamily lending program, at $248.9 million.

General Fund

The General Fund is unique in that it is fed by a variety of revenue sources and is also spent on a range of programs. We reviewed where General Fund revenues come from in the first post. Now let’s look at how they’re spent.

Breaking it out by service, about half of the General Fund is spent on Public Safety, and more than 20% is spent on Administration.

Breaking it out by department, approximately three quarters of the General Fund is allocated to

- Seattle Police Department,

- Seattle Fire Department,

- Human Services Department,

- Finance General,

- Parks & Recreation.

Breaking it out by program, about one-quarter of the General Fund in spent on:

How has the Operating Budget Grown?

In writing the 2025 budget, the City conducted an analysis of each department’s budget over the past five years, charting the growth of each policy area between 2019 and 2024.

Overall, it found that the operating budget has grown $1.7 billion between 2019 and 2024, a 29% increase.

By policy area, the City’s analysis found:

- Livable & Inclusive Communities increased by 174%

- Education and Human Services increased by 65%

- Administration increased by 33%

- Arts, Culture & Recreation increased by 28%

- Utilities, Transportation & Environment increased by 17%

- Public Safety increased by 16%

We can use Open Budget to understand why Livable & Inclusive Communities increased by 174%. Check out how in this explainer:

Across all 6 policy areas, however, the City’s five-year budget analysis attributes the $1.7 billion growth in the operating budget primarily to “baseline and technical adjustments responding to historically high inflation rates.”

Specifically, “increases in personnel costs including wages, healthcare, and industrial insurance (workers’ compensation), internal service costs (e.g., IT support, facilities, and fleet services).”

In other words, a good portion of the increases do not enhance services (with the exception of the multifamily housing program detailed above). We’re paying more money for roughly the same programs and people. How much more? $638.3 million more between now and 2028.

As the Mayor’s Office notes: “In 2023 and 2024, the City ratified labor agreements with the Coalition of City Unions, the Seattle Police Officers Guild, and other labor partners. A large share of the City’s General Fund budget is spent on labor (about 53% percent). These labor agreements therefore increased the City’s cost of doing business.”

This is especially true in the General Fund – and, with unsustainable ongoing growth, is especially problematic. We explain why:

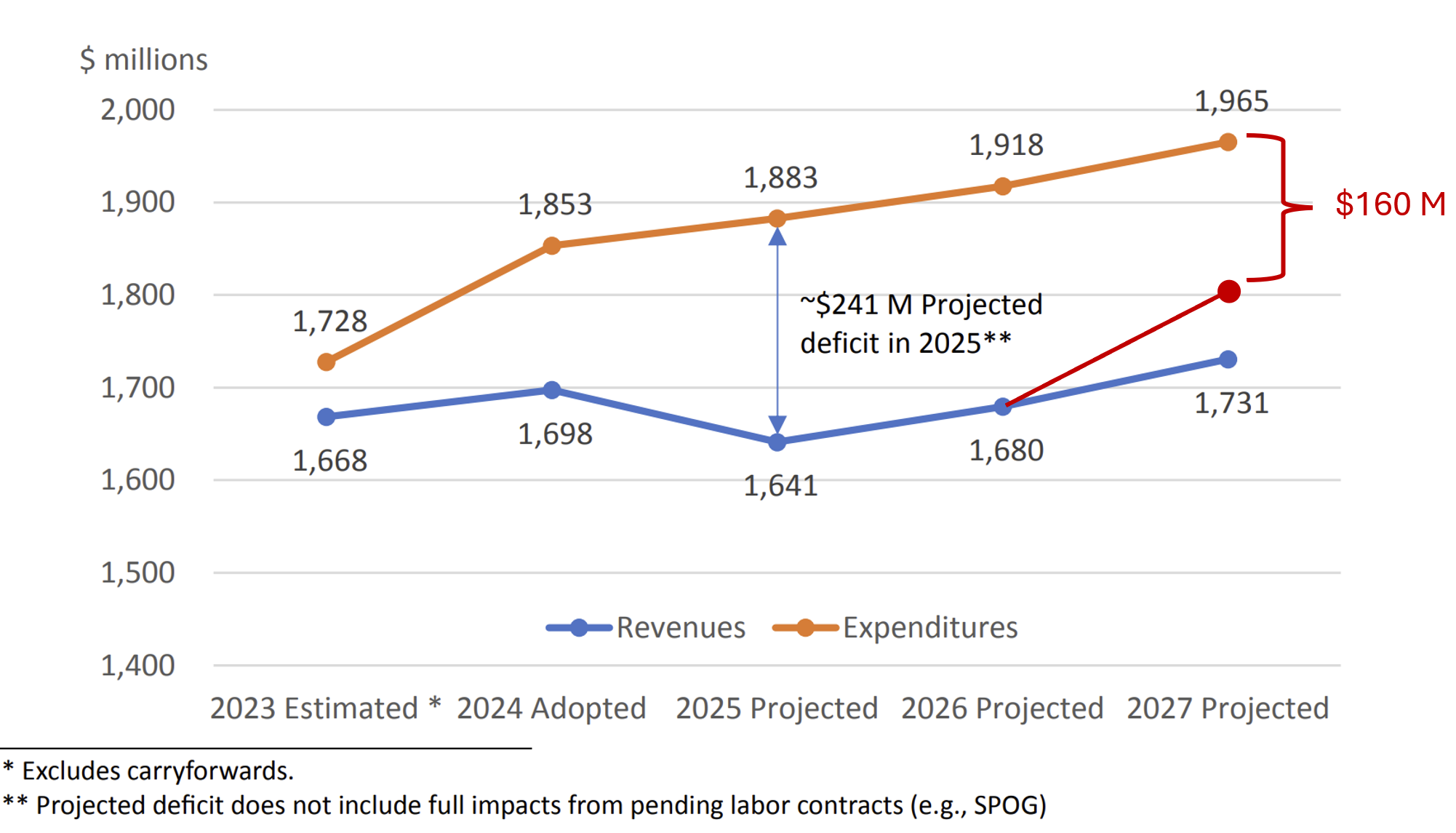

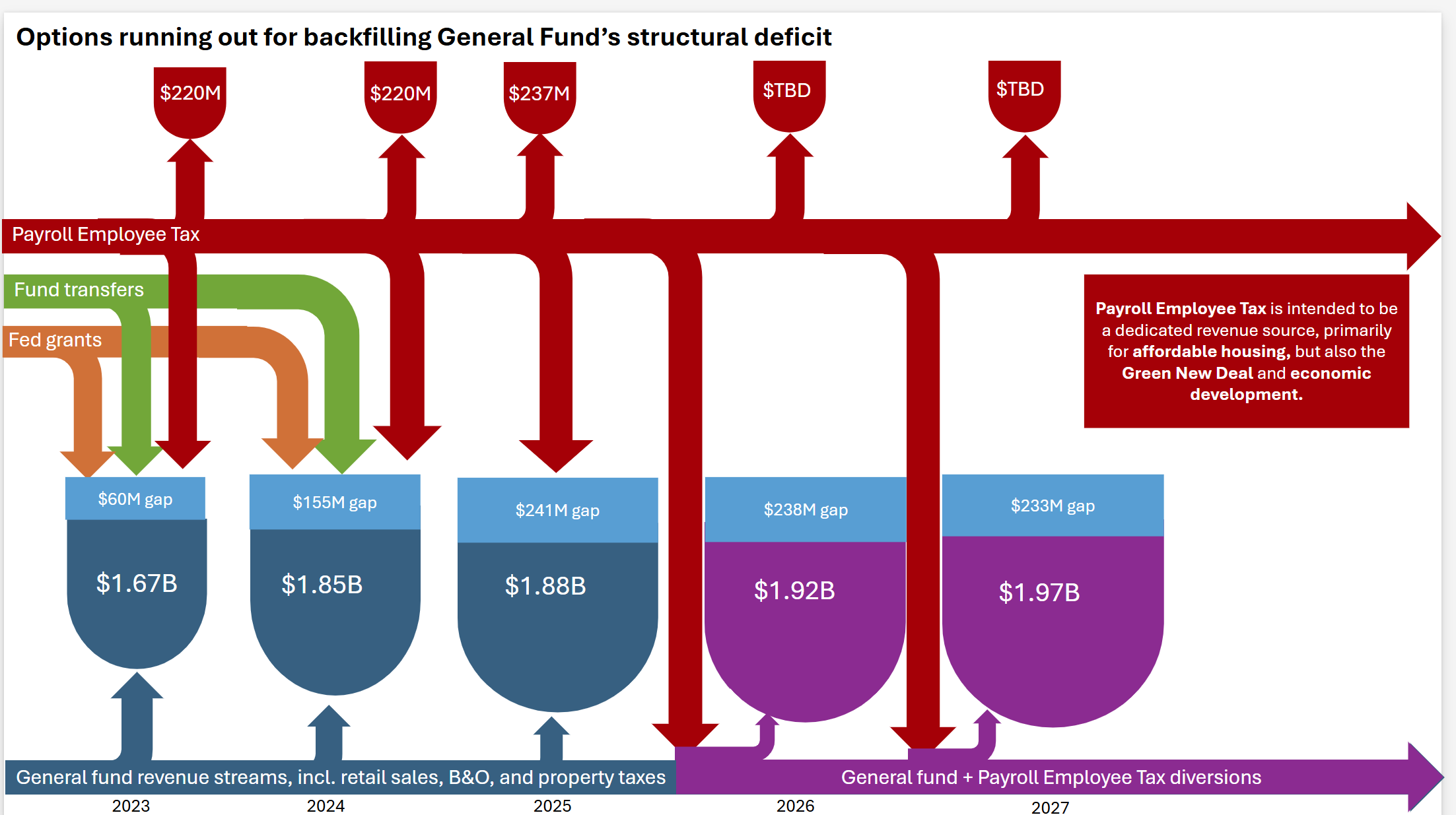

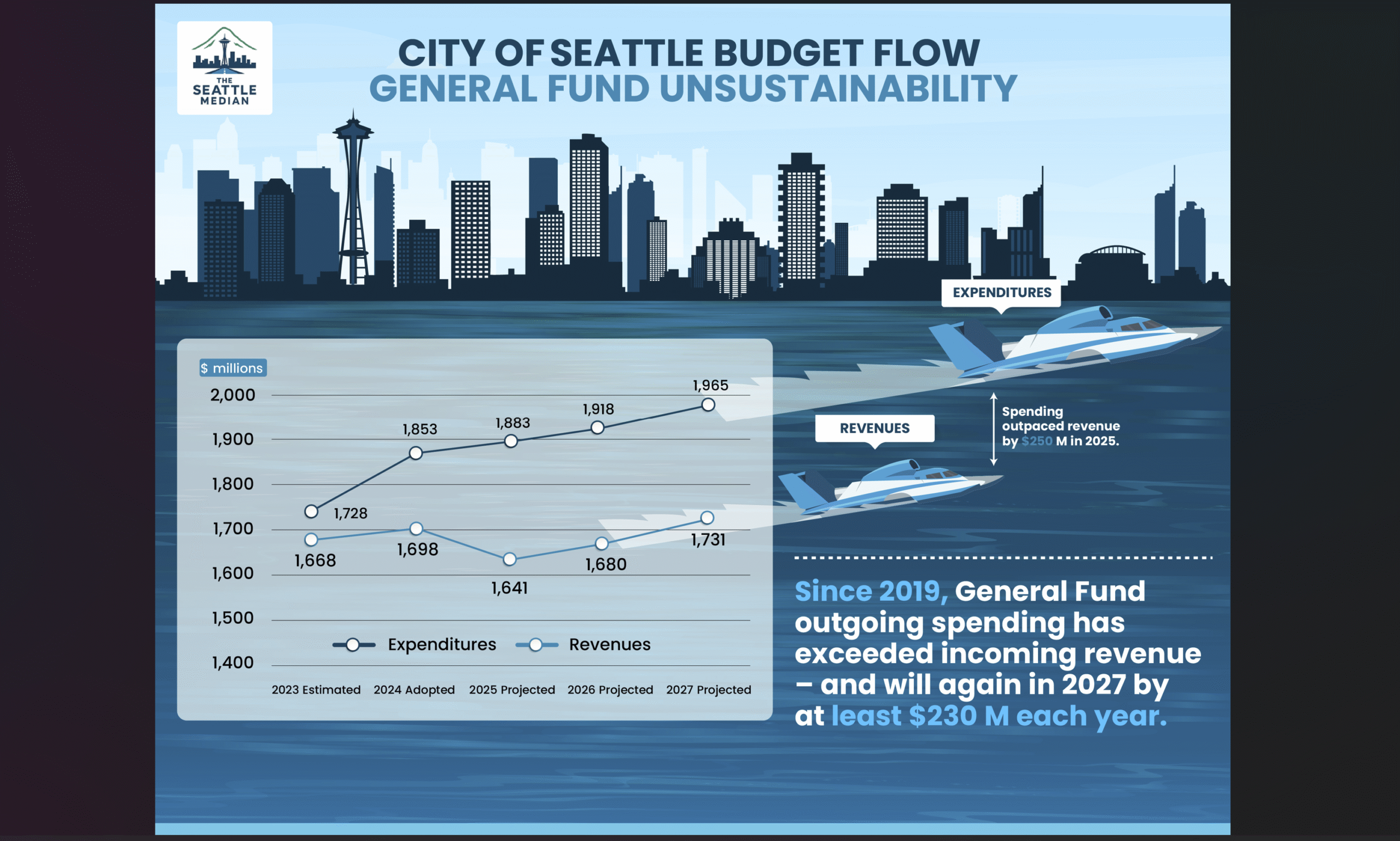

Over the past two budget cycles, budget writers have reported on what they call a “structural deficit” in the General Fund. This is another way of saying that ongoing spending regularly exceeds incoming revenues, which has been the case in the General Fund since 2019 and is projected to continue.

Keeping with water as our visual metaphor, a structural deficit is easier to picture than it sounds:

What is the City Doing About the Unsustainability of the General Fund?

The last time spending from the General Fund was aligned with revenues coming into the General Fund was 2019. Since then spending going out of the General Fund has exceeded revenues coming into the General Fund by ever-increasing amounts, reaching $241 million in 2025.

In the 2023 and 2024 budgets, the City used one-time measures to close this gap, including using fund balances from the prior year, fiscal reserves, federal grants, and other maneuvers.

But mostly they raided the Payroll Expense Tax Fund. As we pointed out in earlier post, the Payroll Expense Tax was meant as a dedicated funding source mostly for affordable housing. Now it’s mostly a fund to backfill the General Fund.

As the Mayor’s Office notes, “Each year since enacting the payroll tax in 2020, the City has balanced the General Fund using a “temporary” allocation of payroll tax revenues. Each of these decisions was made for a one-year period, with the assumption that the payroll tax would no longer be used for this purpose in the following year.”

But that assumption appears to be no longer held.

To address the $241 million gap between incoming revenues and outgoing spending in the 2025 budget, the City diverted $305 million in tax revenues from the Payroll Expense Tax Fund, which represented the largest expenditure from the $516.66 million fund.

Following the budget’s adoption, City budget leaders began including the Payroll Expense Tax Fund in with the General Fund in their General Fund revenue projections, although they are separate funds. Even with this change to count the General Fund and the Payroll Tax as a combined resource, the General Fund is projected to spend $233 million more than revenue coming in, beginning in 2027.

The Council proposed and unanimously approved a “rebalancing” of the City B&O tax, which has been signed by the Mayor is projected to raise $80 million per year if approved by voters.

Even if we adjust the revenue line from $1.73 billion to $1.81 billion to reflect the additional $80 million per year, there is still a deficit of around $160 million.

Budget writers note that the B&O change would make the tax base more volatile and would adversely affect Seattle businesses. They note that a third of the tax burden “would be imposed on 65 taxpayers that paid 87% of payroll expenses tax in 2024.” They also note that this tax is especially risky with a “50% chance of national recession in next 12 months.”

The question remains: How long can the City of Seattle continue to operate on one-time fixes, accounting maneuvers, and unsustainable measures? What would it take for the City to reckon with fiscal reality? What will happen if it doesn’t?

We’ll take up these questions in future posts.