In previous posts, we looked at the performance of the Seattle Housing Levy, while acknowledging that these funding mechanisms are only one part of Seattle’s broader approach to housing affordability.

Seattle’s affordable housing market is shaped by a constellation of forces. Developers, financing, and regulations sit at the core, while land costs, construction prices, political choices, and market demand all influence what gets built, where it goes, and who it ultimately serves.

In this post, we’ll focus on the major players and financing options in Seattle’s affordable housing landscape, which together form the foundation from which housing needs are either met or left unmet.

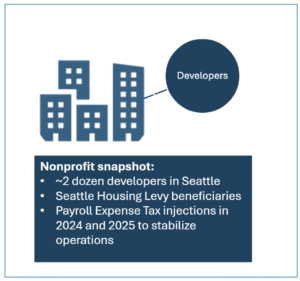

Nonprofit Developers

In Seattle, nonprofit affordable housing developers are the lead actors in the affordability market. A couple dozen organizations fit this description including long-standing developers like Bellwether Housing, Mercy Housing Northwest and Community Roots, which deliver mixed-income and deeply affordable apartment communities.

Nonprofit developers build housing tailored to different segments of the community: senior housing near transit, family housing with services, mixed-income projects with resident support spaces, culturally-specific housing and services and transit-oriented developments adjacent to light rail stations.

Many, if not all, are represented by the Housing Development Consortium (HDC), a regional association of over 200 nonprofit developers, housing authorities, financial institutions, social service providers and advocates working to advance affordable housing policy. Members of the HDC represent the lion’s share of the region’s affordable housing ecosystem.

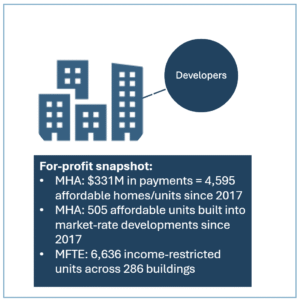

For-Profit Developers

For-profit developers play a role in mitigating affordability issues by mandate and by incentive.

On the mandate side is the Mandatory Housing Affordability (MHA) program, which requires most new residential and commercial development to include either affordable units or contribute fees that fund affordable housing elsewhere.

Under MHA, for-profit developers building market-rate apartments often provide a small share of below-market units on-site or make payments into the city’s affordable housing fund. Those payments are then pooled with other public and philanthropic dollars to subsidize nonprofit developments that serve deeper income levels.

On the incentive side is the Multifamily Tax Exemption (MFTE), which offers a property tax exemption on new multifamily buildings. In return, developers must set aside a certain number of rent-restricted apartments for income-eligible households. For each project, developers can only participate in MFTE or MHA, not both.

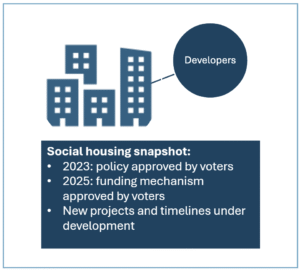

Social Housing Developer

Seattle’s emerging Social Housing Developer represents a newer approach to affordability in the local policy landscape.

Designed to function as a public, mission-driven builder and owner of housing, this model aims to create mixed-income social housing that remains affordable, in contrast to models that rely on expiring tax credits or private ownership cycles.

Voters first approved the social housing developer concept in 2023 and then a dedicated funding stream in 2025.

Although project details and implementation timelines are evolving, the core idea is to treat housing like public infrastructure.

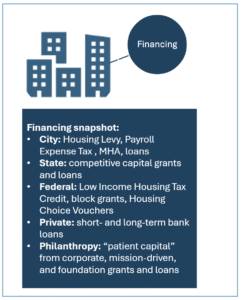

Financing

Multiple funding sources often make affordable housing projects feasible, including federal Low-Income Housing Tax Credits (LIHTC), the Washington State Housing Trust Fund, and the Seattle Housing Levy.

Most public funding is used for construction and acquisition, but in limited cases public dollars also support ongoing operations. Federal rental assistance, for example, funds Housing Choice Vouchers, which help extremely low-income households afford rent and allow some developments to operate sustainably over time.

At the city level, Seattle leaders have responded to recent operational instability among affordable housing providers, driven by inflation and lost rental revenue. In 2024 and 2025, the City injected emergency funds of $14 million and up to $28 million, respectively, from the Payroll Expense Tax to help cover operating expenses and prevent the loss of affordable housing assets.

In recent years, large employers and philanthropic organizations have also stepped into Seattle’s affordable housing landscape, not as direct builders, but as providers of flexible, catalytic capital that fills gaps in traditional financing.

One prominent example is the Evergreen Impact Housing Fund (EIHF), which makes low-cost, long-term loans to affordable housing projects that already rely on federal tax credits and tax-exempt bonds.

This model grew out of Seattle’s 2014 Housing Affordability and Livability Task Force, which found the region lacked patient, flexible capital for large-scale developers. EIFH helps close the gap with long-term, low-interest loans targeted to projects that might otherwise struggle to secure conventional financing.

Conclusion

Seattle’s affordable housing system is not defined by any single program, developer, or funding source. Instead, it is the product of how nonprofit, private and public actors interact with policies, financing tools, and market conditions over time.

In future posts, we’ll examine these components in greater detail—looking more closely at how nonprofit developers perform, how inclusionary policies like MHA and MFTE translate into housing on the ground, how the Social Housing Developer evolves, and how public, private, and philanthropic financing tools shape what ultimately gets built.