In a previous post, we mapped out Seattle’s complex affordable housing landscape: nonprofit developers, private development mandates and incentives, public and private funding streams, and now a new social housing model, all aimed, in different ways, at addressing affordability.

What Seattle does not have is a single affordable housing system with shared goals and feedback loops. Instead, it has an ecosystem: a collection of tools and actors, each optimized for a specific purpose, operating alongside one another but not always in coordination.

To understand whether this ecosystem is working, the most useful lens is not intent or effort, but outcomes. How many units are being produced? Who is being housed? At what income levels? And how stable are they over time?

Looking at those outcomes can help us track over time whether policies are moving the needle.

Outcome #1: Unit production

By one of the most commonly cited measures, Seattle’s affordable housing ecosystem is lagging behind the broader need. According the City’s comprehensive plan, Seattle needs to generate 4,480 affordable housing units per year between 2019 and 2044 to keep pace with population growth.

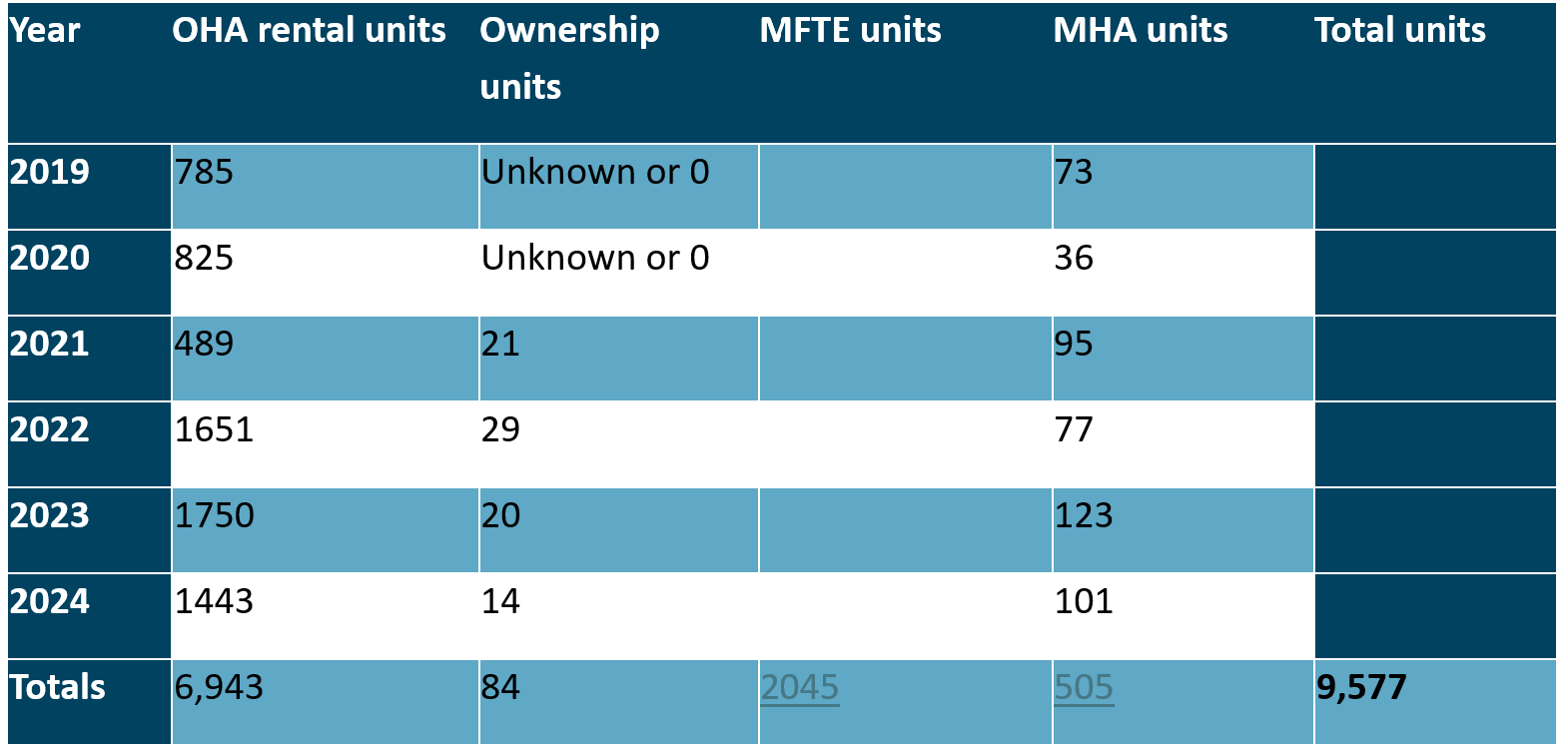

The most recent annual reports from Seattle’s Office of Housing show nonprofit developers and private developers have added thousands of income-restricted homes in Seattle since 2019 but the average falls well short of the need: ~1,600 units per year.

The chart below shows Office of Housing-funded rental units; permanently affordable housing units sold to income first-time homebuyers; Multifamily Tax Exemption units; and Mandatory Housing Affordability units under the “performance option” (vs. the payment option which is counted as part of the Office of Housing numbers).

A substantial number of new income-restricted units in recent production cycles have been set at upper affordability bands — often near or above 50–60% of Area Median Income — and the bulk of those units were studios or one-bedroom apartments, as reflected in MFTE program outcomes showing that fewer than 13% of newly made available MFTE units had two or more bedrooms.

These choices were not accidental. Building smaller units for higher-earning eligible households allows projects to charge higher rents within program limits, require less subsidy per unit, and maximize unit counts with limited public dollars. Over time, those incentives shaped what was built.

The result was a significant expansion of what is often called “workforce housing”: homes intended for people with steady incomes who are priced out of the private market but are not among the city’s lowest-income residents.

Outcome #2: Occupancy

This workforce housing explosion has had unintended consequences, as reported by The Seattle Times this year.

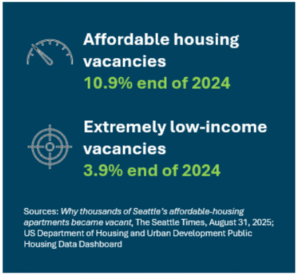

The Times reported on state compliance data submitted to the Washington State Housing Finance Commission, which showed vacancy rates in income-restricted housing rising sharply. At the end of 2024, vacancies of publicly funded units sat at 11%, up from the low 2% range a decade ago. Why?

Rents in subsidized housing are set by income-based formulas, not by comparison to nearby market prices. During the 2010s, when market rents were rising rapidly, these units were consistently cheaper than private alternatives, and demand far exceeded supply. But as market rents softened in recent years — particularly for studios and one-bedroom apartments — that gap narrowed, and in some cases disappeared.

For households near the top of the eligibility range, the calculation is straightforward, hold the Times reporting. If a market-rate apartment across the street costs the same or less, and comes without additional paperwork or restrictions, the incentive to remain in income-restricted housing diminishes.

Outcome #3: Meeting needs

At the same time that some workforce housing sits empty, Seattle continues to face an acute shortage of housing affordable for people with extremely low incomes, including those experiencing homelessness. Seattle Housing Authority, which oversees the city’s lowest-income housing stock, shows wait times for SHA units ranging from one year to 12 or more years. At the end of 2024, the vacancy rate for SHA units was just shy of 4%.

The buildings now facing higher vacancy rates were not designed to serve households earning 0–30% of Area Median Income, nor were they intended to absorb people living unsheltered. They lack the deep rental subsidies and service funding required to operate sustainably at that level. Federal rental assistance, such as Housing Choice Vouchers, remains limited relative to need.

The result is a stark juxtaposition: vacancies at the upper end of affordability alongside severe unmet need at the lower end.

Outcome #4: Operational stability

The vacancy story also intersects another outcome: the financial stability of affordable housing providers themselves.

Public funding has historically prioritized construction and acquisition. Operating revenue for affordable housing — largely dependent on capped rents and limited rental assistance — has not kept pace with rising costs and loss of rental revenue. The pandemic accelerated these pressures, leading to widespread financial strain across the sector.

In response, the City allocated $14 million in emergency operating support from Payroll Expense Tax revenues in 2024. The injection was labeled a one-time emergency measure, but it was duplicated and doubled in size in 2025. The stated goal is to stabilize affordable housing providers and prevent continued divestment of affordable housing stock.

Looking ahead

In future reporting, we can continue to track outcomes across Seattle’s affordable housing ecosystem, examining how different approaches perform over time and how changing conditions shape the results. That broader view is essential to understanding what the city’s housing investments are producing — and what they leave unresolved.